There are four factors that will determine your premium for health care reform plans.

Age

Smoker

Geographical Location

Income

No longer will health questions be required. However, I believe the most confusing factor will be your income. Income will determine what subsidy will be available to offset your premiums. The chart below will give you an idea of what income limits will be considered during ACA to determine who qualifies for a subsidy.

2013 Federal Poverty Limits (FPL)

# Person in

Household

100% FPL

150% FPL

200% FPL

250% FPL

300% FPL

400% FPL

1

$11,490

$17,235

$22,980

$28,725

$34,470

$45,960

2

$15,510

$23,265

$31,020

$38,775

$46,530

$62,040

3

$19,530

$29,295

$39,060

$48,825

$59,590

$78,120

4

$32,550

$35,325

$47,100

$58,875

$70,650

$94,200

As you can see above, a family of 4 with an income of $94,200 or less will qualify for some sort of premium subsidy and vice versa a family of 4 with income greater than $94,200 will not receive a subsidy.

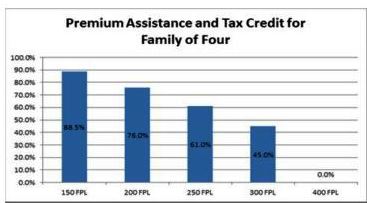

So now we have determined who will qualify for a subsidy, now how much will you receive? Unfortunately I can't answer that exactly at this time because the amount will be based on a percentage of the premium. The chart below will show what percentage of the total premium your subsidy will be based on a family of four and where you fall in the income scale.

For example, a family of 4 that makes $70,650 (300% FPL) will receive a premium subsidy equivlant to 45% of the annual health insurance premium. Rates are being filed with the Department of Insurance now by the various carriers. We should have a better look at what premiums will look like in the coming months.

In March of 2010 Congress passed the Affordable Care Act (ACA). Some parts of the law have already been implemented but the majority will take effect in 2014. These include:

Individual mandate to purchase health insurance (coupled with federal subsidies for individuals and families that qualify based on 2012 income. Estimate 2/3 North Carolinia's uninsured will qualify)

Insurers must accept ALL applicants, regardless of health status Guarantee Issue

Eliminate medical underwriting cannot rate due to health status

Pre-existing conditions covered without waiting periods or exclusions

Community rating limits premium to a person's age to no more than 3:1 ratio

Maternity covered on all plans

Establish Exchanges for individuals to purchase health insurance

Initial Enrollment for 2014 coverage through the exchanges will begin October 1, 2013 and end March 31, 2014.

The part that I feel will affect most people that live in North Carolina will be rates and subsidies. Lets look at each briefly:

Rates:

As noted above above plans will be guaranteed issue, no rate ups, community rating, and maternity covered on all plans. All these will impact rates when compared to what they are today. Think about it, a person with Cancer will be paying the same rate as a person that runs marathons and is in the best shape of their life. Having a higher claim ratio will make rates increase. My understanding from various carriers is that we can expect rates to be 35-50% higher than they are today.

Subsidies:

So most will see an increase in rates but also most will have these rates offset by a Governement subisdy. According to one carrier, approximately 2/3 of the current uninsured North Carolinians will qualify for the subsidy. This will be based on your 2012 income and will be available for individuals and families under 400% Federal Povery Level (FPL). To put this in perspective 400% FPL for a single individual is $45,960 and for a family of four it would be $94,200.

As you can gather some people are going to get hit a lot harder than others and on the flip side some people are going to get a much better "deal".

As we continue to learn more about the changes ahead we will continue to bring you more information.

In 2013, North Carolina Health Savings Account (HSA) plans will see in increase in both their contribution limits as well as their deductible minimums.

The maximum contribution that can be made to your HSA account will now be $3,250 for individual accounts and $6,450 for family accounts. The individual limit is $150 higher than 2012 and the family limit is $200 higher than 2012. This gives you more money to put away for medical claims which also means more money to write off on your taxes. Remember, ALL money you put into your HSA account, up to the maximum allowed, is 100% tax deductible whether you use the money or not.

Also, in 2013 the minimum deductible allowed for an individual plan is $1,250, which is a $50 increase from 2012. Also for two or more persons on the policy, known as a family plan, the minimum deductible will be $2,500. Most of the time, it is not advised to go with these low of deductibles as the annual premiums for these are higher than savings you would get if you were to max out the deductible. In otherwords, you will typically save money with a higher deductible whether you used the coverage or not.

One of the drawbacks of Health Care Reform (HCR) is that it has caused almost all health insurance carriers in North Carolina to discontinue issuing child only policies. Why? Because part of this reform is that no child under the age of 19 can be denied health insurance due to pre-existing conditions and the insurance carrier cannot put exclusion riders on children. This means that children are guaranteed issue which puts a lot of liability on the carrier.

North Carolinians have an option though that many states do NOT offer children only health insurance policies. The states largest insurer will still issue coverage without an adult being on the policy with them. Although coverage cannot be denied nor any exclusions placed, carriers can still increase rates based on pre-existing conditions.

I get calls all the time from people looking for new health insurance because they claim one of two things:

"I don't understand why my rates keep going up, I haven't had any claims"

"My rates went up significantly at renewal because I filed a few claims last year"

Let's examine this. First off, individual health insurance carriers by law CANNOT raise your rates due to claims. Whether you filed a $100 claim or a $100,000 claim this will NOT effect your rates. Auto and homeowners insurance rates can and do increase based on rates...don't get them confused.

Rates do typically rise every year for health insurance. However, due to health care reform laws recently inacted we are seeing much lower annual rates increases than in the years past. So, why did your rates go up? Let's look at the main reason for rate increases:

Cost of living increase. In other words...inflation. Everyone in the entire area would get this rate increase.

Age. Most carriers have age brackets for rates. If you happened to age into a new age bracket (example 55-59 bracket to the 60-64 bracket) you can see a significant jump...typically between 10-20%.

Claims based on the block of business. Carriers will look at the premiums in versus claims out for a geographical area. If a trend is seen then they will adjust rates for everyone in that area. This could be critical if you are with a lesser known carrier that has a very small block of business.

Those are typically the reasons why individual health insurance rates will increase annually. You should contact your agent when your plan renews to make sure that you are still in the best plan that meets your needs.

It's been a while since I posted a blog article but I saw something on Dateline the other night that hit a nerve and one that I end up talking to potential clients often about. If you are looking for Medical Insurance North Carlolina, PLEASE make sure that you talk with a state licenced insurance agent.

There are numerous companies out there that prey on individuals with pre existing conditions or just people looking for affordable health insurance in North Carolina. These plans are often referenced as Limited Benefit Health Insurance. The word Limited is an understatement. In my opinion, you are better off putting the premiums that these plans cost under your mattress than pay for this...your money will go further.

Typically these plans will pay a set amount for particular services. For example I have seen some that advertise:

up to $250 per day for hospitalization....a one night stay in the hospital will likely run you close to $1000 or more per day.

up to $500 per day for intensive care....this will likely be closer to costing you about $4000 per day.

up to $400 for out patient surgery...my dad recently had outpatient surgery for kidney stones and his bill was $28,000! Luckily he has Major Medical Insurance North Carolina!

As you can see, these aren't really "benefits". And to top it off you are paying $200-500 per month for this garbage. It really makes my blood boil that folks out there can sell this stuff to people and sleep easily at night. Just remember, if it sounds to good to be true it likely is.

Here are some common marketing tactics that these companies will say:

You are pre approved at a rate of $$.

All pre existing conditions covered, no underwriting.

This plan is only available for the next 3 days so please call me back asap

If you hear or see any of this nonsence...RUN!

Just remember when shopping for major medical insurance North Carolina that you use a licenced insurance professional...we are here to help you find the best plan (NOT the most expensive). There are numerous plan options avaiable that we can explain to you to find coverage that meets what you are looking for. Here is a copy of my NC License...whether you buy from me or someone else make sure they can produce one of these for you.

Here is the video series from Dateline (sorry about the ads)...it's well worth watching to make sure you don't fall victim to this type of nonsence.

If you are looking for NC dental insurance there is a new player in town. Cigna North Carolina is now offering a comprensive dental plan that can be added on when you purchase one of their health plans. This is not a stand alone plan - meaning that you cannot buy their dental coverage by itselt...you have to have one of the medical plans as well. However this is a pretty good plan that will stand toe to toe with the others available, actually will out perform them in many others. Here are how the benefits stack up (in network):

Calendar Year Deductible per Person $50

Calendar Year Maximum per Person $1,000

Preventive/Diagnostic Services (no waiting period) Cigna Pays 100% (no deductible)

Oral Exams

Routine Cleanings

Routine X-rays

Fluoride Application

Sealants

Space Maintainers (non-orthodontic)

Basic Services (6 Month Waiting Period) Cigna pays 80%

Fillings

Non-Routine X-rays

Emergency Services to Relieve Pain

Oral Surgery, Simple Extractions

Major Services (12 Month waiting Period) Cigna pays 50%

Crowns/Inlays/Onlays

Root canal Therapy/Endondontics

Minor Periodontics

Major Periodontics

Oral Surgery, All Except Simple Extractions

Surgical Extraction of Impacted Teeth

Relines, Rebases, and Adjustments

Repairs - Bridges, Crowns, and Inlays

Repairs - Dentures

Anesthetics

Dentures

Bridges

There you have it. Comprehensive Coverage at an affordable price. Here are the rates for 2011 in Mecklenburg County (prices vary by area):

Everyone that is looking for health insurance in North Carolina should also be looking for the BEST health insurance. There is no one size fits all. What is right for you may not be right for your neighbor. Here are some tips to assist you in what you are looking for.

The primary tip you should look at is how often your family uses healthcare related services on an average year. Some folks may visit their physician each month. Whereas others might only see their physician annually for their preventative physical. These two types of individuals would need completely different plans. For those that use medical services on a regular basis you may want to pay a little more for full comprehensive coverage so that you have copays to cover your routine visits and prescriptions. Whereas if you are generally healthy and only want to see the doctor when you have to you may look for a less comprehensive coverage like an HSA plan to cover you for the catastrophic scenario. However, in each case you still have to weigh the price vs benefits ratio.

The next suggestion in getting the best health insurance in North Carolina is refelective upon your budget. Health insurance is expensive.. Nevertheless, there are plans available that can save you a lot of money. You could take a plan that has a higher deductible each year and this will greatly affect you monthly premiums. As mentioned above, a high deductible health plan (HDHP) paired with a health savings account is now a very comom choice for affordable health insurance.

The last tip for securing the best health insurance in North Carolina your family is to utilize the services of a good health insurance broker. Most people think that they will pay more when using a broker.This IS NOT the case. In North Carolina, insurance companies cannot charge more for insurance policies that are bought through a broker. By taking advantage of the knowledge of a qualified broker you will likely save much more money that you would trying to do this on your own.

North Carolina, like many other states, is still struggling with high unemployement. Most individuals in our state have relied on their employer for the NC health insurance benefits. Now that so many people are still out of work many are finding that they cannot afford their COBRA health insurance premiums...especially if they have recently lost the COBRA subsidy that was put in place in 2009 with an extension in 2010.

So, where does that leave you? Well there really are better choices than COBRA to begin with. Because COBRA only last for up to 18 months it really is only a temporary solution, albeit an expensive one.

What type of coverage is best for you and your family? I can't really answer that here as it really is dependent on your current situation. More times than not I find that a high deductible health plan works the best for folks that are generally healthy and are looking to save on their premiums but still have full catastrophic coverage for hospitalizations and prescriptions.

Sometimes you can save even further with a "Basic" type plan. These typically limit the number of office visits anywhere from 2-4 times per year depending on the carrier, limit prescription coverage to only generic drugs, but will still offer you great coverage in the event you are hospitalized. (Note, due to the generic only drug coverage, I personally have a lot of reservations about these. Some prescriptions can cost $2000-$4000 per month if you happen to be the unlucky one that has to take them you wont be real happy with this plan).

Another option is a short term policy. These are often very inexpensive and they do not cover office visits, prescription drugs or preexisting conditions. The only time I find these to be a useful option is if you have guaranteed issue coveage (like an employer plan) starting in the next 3-6 months and you use this as "gap coverage".

You can always give me a call at 704-560-8972 to discuss your options. This is a free service and I will explain to you all your option or rates. Or if you would like to just see some of your options, click this link for your North Carolina health insurance quote.

As you can see from a lot of my blog posts and my website, I am a pretty big advocation of having a health plan that qualifies for a North Carolina health savings account.

Starting January 1, 2012 for High Deductible Health Plans (HDHP) the annual contribution limit for health savings account will increase. Currently for individuals with self-only coverage enrolled in an HDHP, the maximum annual contribution amount will increase from $3,050 to $3,100. For individuals with family coverage (2 or more on plan) the contribution limit will increase from $6,150 to $6,250.

No changes are being made as to what defines a HDHP. Currently and into 2012 an HDHP is defined as having an annual dedcutible for self-only coveraeg of at least $1,200 and a $2,400 deductible for family coverage. In addition, for self-only coverage the annual out of pocket (OOP) maximum cannot exceed $6,050 (most carriers cap self-only OOP at $5,000) and $12,100 for family coverage (most carriers cap family OOP at $10,000).

Please review your options for North Carolina health plans and contact us to assist in determining which plan is right for you.

Subscribe

Subscribe